If you have extra cash on hand, consider how that money could be best used to meet your financial goals. That may mean paying down your mortgage quicker … or not. Let’s explore the advantages and drawbacks to that strategy and how to decide if it’s right for you.

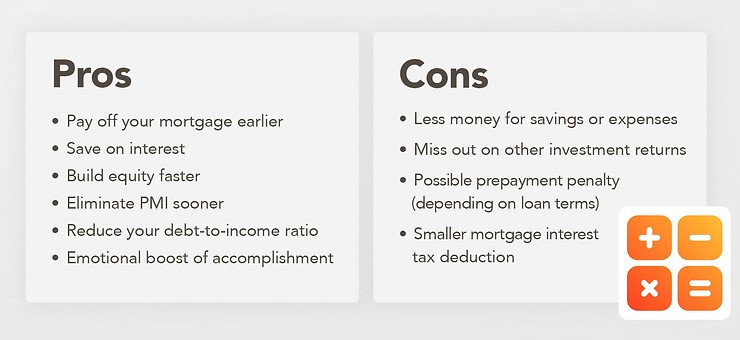

Looking at this list of pros and cons, it’s clear that there’s no one right answer. The key concept to consider is opportunity cost: In other words, what do you give up in order to make extra payments? Your mortgage is only one part of your financial health, so before you pay extra money toward it, look at these other factors:

- Debt. If you’re carrying a lot of credit card debt, you’re probably better off using extra cash to pay that down. Your mortgage may be accruing 7% interest, but your credit cards are likely charging much higher rates. Reducing credit card debt is also a proven way to boost your credit score.

- Emergency Funds. A recent study showed that nearly half of Americans have less than $500 in savings,[1] which means they might struggle to cover an unexpected car repair or medical bill. Financial experts recommend saving enough to cover three to six months of living expenses.

- Retirement Savings. Are you maxing out retirement contributions, especially if you have an employer match program? No one likes to pay interest, but earning interest is always in your best interest, especially in long-term accounts like 401(k)s and IRAs.

When making mortgage prepayments, you must specify that you want the extra payment to go toward your principal balance.

What About Investing?

If you’re not carrying high-interest debt, have healthy savings, and are adequately saving for retirement, there’s a fourth opportunity cost to consider: possible investment returns. Here’s where risk tolerance comes into play. Are you okay with potentially losing money — at least in the short term — or are you looking for a safe bet?

There are no guarantees with the stock market, but it has historically provided good returns over time. Depending on interest rates, housing market values, and other factors, you might make more money investing than you would prepaying your mortgage.

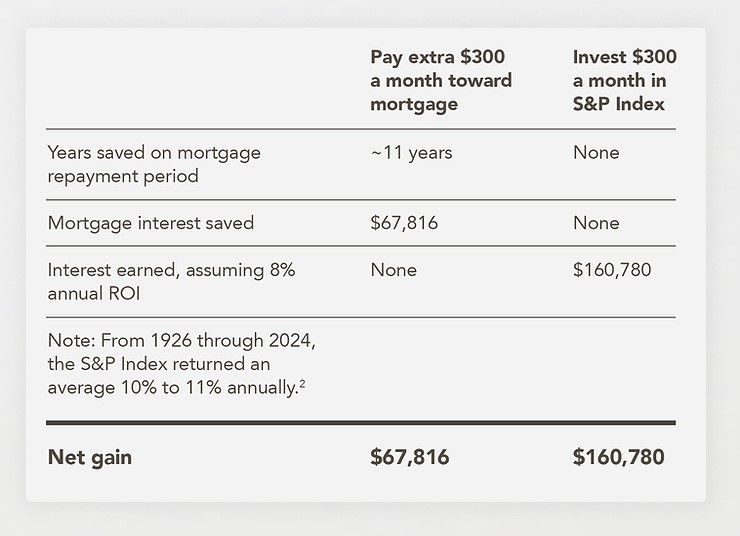

Here’s a sample scenario using a 30-year mortgage of $200,000 at a fixed rate of 4.5%. After 19 years, here are the results:[2]

In this scenario, the investment return is more than double the mortgage interest saved, so the homeowner would be considerably better off investing that $300 a month. But again, the stock market can be unpredictable, and you don’t necessarily know how long you’ll stay in your home. Keep in mind, this is just one scenario. You could also make lump-sum payments, make bi-weekly extra payments, or pay an even higher amount per month. Your results will also be dependent on your mortgage rate and loan balance.

Another Option: Refinancing

If using your extra money to invest appeals to you, but you still want to reduce the amount of interest you pay on your home loan, refinancing may be an option. You could switch to a shorter loan term, or you may be able to keep the same term and refi to a lower rate.* Talk to a home loan professional to help you run the numbers and see if refinancing is a good fit for your financial goals.

*This is not a commitment to lend. Not all borrowers will qualify.

The information in this article is for informational purposes only and should not be interpreted as financial advice. Consult a financial advisor for more information.

Used by permission from Vibrant Living.

Sources:

GOBankingRates, “How Much Money Do Americans Have in Their Bank Accounts in 2024?” June 27, 2024.

Forbes Advisor, “Pay Off Mortgage or Invest: What Does the Math Say?” June 26, 2024.